The US healthcare industry is primarily private. Even Medicare has vast private company ties. Medicare Advantage (Part C) is run by public healthcare companies. Medicare Prescription Drug Coverage (Part D) is also run by public companies. Even basic Medicare Parts A and B are administered and disbursed by contracted companies (these companies include Noridian, Palmetto, Novitas, and other companies that you may never have heard of).

These companies necessarily are profit-oriented to produce earnings for investors, and to provide funds for administration and expansion.

Many argue that this system, profit-driven, unavoidably increases prices. On the other hand, the need to maximize profits also drives efficiencies in administration, as government is notoriously inefficient.

However, it is not my concern in this essay to argue for a change to the current system. It is beyond my scope here to create a path to what one might prefer; it is instead to examine what is possible and practical.

There are two basic ways to move out of a for-profit healthcare system. The first is to socialize healthcare. Countries that have adopted socialized healthcare use government funds to deliver healthcare services by owning hospitals, clinics, and employing the medical staff. Citizens receive treatment without upfront costs. Doctors and nurses are paid a salary rather than a fee for each service they deliver, each test they order, or each procedure they do. This limits outlays as those healthcare providers’ costs are fixed.

Most industrialized countries currently have socialized healthcare including our neighbors Canada and Mexico. In Europe, virtually all countries including the UK, Austria, Denmark and all other Scandinavian countries, Finland, Ireland, Italy, Portugal, Spain, France, Switzerland and Germany. Around the world Australia, China, Israel, Japan, South Korea, New Zealand, etc., also have socialized healthcare.

“Universal Health Care is so hard to do, that only 66 of the 67 industrialized countries have figured out how to do it.”

However, if the US were to try to convert its current system into a socialized system, we would need to nationalize all hospitals and clinics and convert physicians from either sole practitioners, or employees of public companies into federalized, salaried, employees. This disruption could have catastrophic consequences, result in the closure of hospitals and clinics and the voluntary retirement of physicians and specialists, cost trillions of dollars to privatize the public companies, and is politically untenable in the foreseeable future.

The second option is to federalize insurance, eliminating all private insurance. This would require huge tax increases to fund, and even if the mathematics would show that the net insurance costs to the public would decrease, the political will would seem to be quite weak.

The option of offering a government-sponsored insurance program to the public to compete with private insurance in the marketplace could garner some support. There are examples of government insurance programs. FEMA offers Flood Insurance to people who cannot get it on the open market. Social Security is a form of retirement insurance. Some states, like Florida created their own homeowner’s insurance (Citizens) to provide lower cost insurance for homeowners whose prior insurance companies left the state. One of the issues with this model is that when insurance companies see the formation of high-risk insurance plans by the state or federal government, they often react by removing those high-risk coverages from their own policies, or make those specifics prohibitively expensive, thereby dumping the high-risk cohort onto those state and federal agencies, thereby making the costs of running those programs significantly higher than initial projections.

For the purposes of this discussion, I find both of these options unattainable. Therefore, we need to look at what drives the current system and how current governmental policies may affect costs to the public.

For a number of years, I was the managing partner of a company that provided consultancy to Pharma companies, device manufacturers, and other healthcare companies. The members of this firm were ex-senior level executives from major healthcare insurers, including senior medical directors, sales executives, financial executives, and technology executives. From this perspective I learned quite a bit about the underlying logic of pricing, approving, and delivering healthcare payments to hospitals, physicians and patients.

The basis of healthcare insurance is mathematical. One thing I heard, over and again, was that “Payers” (the term used in the industry to represent the insurance companies) are willing to cover anything the customers want. True. However, each item covered comes with an associated cost.

The most important people in any insurance company (and this applies to home insurance, car insurance, and health insurance also) are the actuaries. It is their responsibility to analyze the economics of coverage. If you live in an area where flooding is more likely than another, then the risks and costs associated with covering water damage from flooding will be higher as will your flood insurance rates. If you drive a car for which parts are expensive compared to other cars, the costs of repairs will be higher as will your auto insurance rates.

Likewise, when a new medication is added to the formulary of a prescription plan, or a new procedure is approved for coverage, the costs of providing that medication or procedure will be reflected in an increase in the costs of providing insurance; and since the costs are distributed over the entire covered population, whether they need or will need that medication or procedure, all rates increase in order to spread the risk over the largest number of insured people as possible.

Actuaries are tasked with determining the risks and costs associated with providing insurance coverage for each line item that is included. Costs may decrease due to a new, less expensive contract with a “Provider” (the term used in the industry to refer to hospitals, clinics, physicians, nurses, etc.), or due to a new cheaper alternative therapy, or the evolution of name-brand drugs to generic substitutes. These changes may allow the actuaries to reduce a particular line-item cost. More often, a new procedure, treatment, pharmaceutical, or apparatus will have been approved by the FDA, and this may result in better outcomes, but increased costs.

A quick aside here. When Bayer introduced the allergy relief medication Claritin, they broke with historical norms, and advertised the medication on TV, Radio and in print media. Their aim was to produce consumer pressure on the physicians to prescribe this medication. They were spectacularly successful. With that barrier broken, Pharma has spent heavily on advertising new medications, increasing the pressure on providers to prescribe those medications even when the benefits are only incremental. Or, when a patent was expiring, the manufacturing company might create a small, put patentable change in the medication allowing them to price it at a higher non-competitive rate. A great example is the creation of Nexium, which is a simple extended-release version of Prilosec. Since Prilosec was becoming generic, and eventually over-the-counter, advertising pressured consumers to demand a prescription for Nexium from their doctors.

The net result is that patented medications drive up the cost of providing treatments to patients, irrespective of the cost/benefit value of those medications.

Americans like to receive treatments. They want prescriptions from their doctors. You do not need an antibiotic when you have a viral infection, but often a physician will prescribe one simply because the patient wants SOMETHING. Overprescribing, over-testing, and excessive treatments all need to be paid for, and the Insurance companies need to build those costs into their premiums.

It is an interesting actuarial truism that if you provide coverage for well-patient preventative care, total costs may actually increase. For example, 50 years ago, a patient with high blood pressure, or high cholesterol may not have had that condition diagnosed, and they may have had a catastrophic heart attack and death. Today, preventative medical screening will likely have diagnosed those underlying conditions, and the primary physician will have treated them with simple, inexpensive medications. The net result is that the patients who would have died (with no further insurance cost exposure), now survive longer and are given time to develop other, more expensive diseases which need to be treated. The net result (simply from the mathematical perspective) is that preventative medicine actually increases the costs of providing medical care to people, and therefore, requires higher insurance rates.

What about health insurance inflation?

It is true that inflation has increased the price of goods and services over the past 25 years. Has Health Insurance followed that increase?

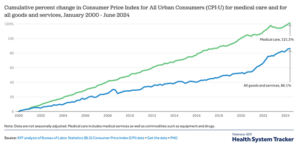

Not surprisingly, based on the arguments above, health insurance inflation has outpaced consumer inflation in general.

As costs have risen, premiums have followed.

Healthcare costs have escalated at a rate greater than that of general goods and services because coverage has expanded as a result of new treatments, diagnostic aids, medications and disease maintenance.

Part II will address how these cost increases might be mitigated.